closed end credit disclosures

The disclosure rules of Regulation Z differ depend ing on whether the credit is open-end credit cards and home equity lines for example or closed-end such as car loans and mortgages. Regulation Z is structured accordingly.

How To Comply With The Closing Disclosure S Three Day Rule Alta Blog

102659 Reevaluation of rate increases.

. Closed end credit disclosures. Closed-End Credit Disclosure Forms Review Procedures. A line of credit is a type of loan that borrowers can take money from over time rather than all at once.

Amount financed 102618b c. The premium may be disclosed on a unit-cost basis only in open-end credit transactions closed-end credit transactions by mail or telephone under 102617g and certain closed-end credit transactions involving an insurance plan that limits the total amount of. In a closed-end consumer credit transaction secured by a first lien on real property or a dwelling other than a reverse mortgage subject to 102633 for which an escrow account was established in connection with the transaction and will be cancelled the creditor or servicer shall disclose the information specified in paragraph e2 of this section in accordance with the form.

T No-guarantee-to-refinance statement - 1 Disclosure. 22620 Subsequent disclosure requirements. 10153D the creditor shall disclose a statement that there is no guarantee the consumer can refinance the transaction to lower the interest rate or.

For a closed-end transaction secured by real property or a dwelling other than a transaction secured by a consumers interest in a timeshare plan described in 11 USC. 4 The amount of any finance charge. 102661 Hybrid prepaid-credit cards.

A Form of disclosures1 GeneralThe disclosures required by paragraph d of this section shall be. For residential mortgages and extensions of credit secured by the members dwelling the disclosures must be provided within three 3 business days after receiving the. Closed-end credit such as an installment loan or auto loan is for a specific dollar.

12 CFR Subpart C - Closed-End Credit. For purposes of this section an annual percentage rate is the annual percentage rate corresponding to the periodic rate as determined under 102614b. Sub-sections a and b cover all types of closed end transactions and then the various following subsections have specific requirements for credit sales for consumer loans for mail or telephone transactions etc etc.

102657 Reporting and marketing rules for college student open-end credit. By contrast open-end credit is revolving credit like a credit card that enables you to borrow repeatedly with no specified repayment date. 22619 Certain mortgage and variable-rate transactions.

2268 is the principal section for closed end credit disclosures. The amount of the down payment expressed either as a percentage or as a dollar amount. This is a sample of the information required on the Closing Disclosure by 102638j for disclosure of consumer funds from a simultaneous second-lien credit transaction not otherwise disclosed pursuant to 102638j2iii or iv that is used to finance part of the purchase price of the property subject to the transaction.

Identity of the creditor 102618a b. 22620 Subsequent disclosure requirements. There are two basic kinds of lines of credit.

Closed-end consumer credit transactions secured by real property or a cooperative unit other than a reverse mortgage subject to 102633 opens new window are subject to the disclosure timing and other requirements under the TILA-RESPA Integrated Disclosure rule TRID. The disclosures required under subsection a with respect to any open end consumer credit plan which provides for any extension of credit which is secured by the consumers principal dwelling and the pamphlet required under subsection e shall be provided to any consumer at the time the creditor distributes an application to establish an. Closed-end credit allows you to borrow a specific amount of money for a finite term.

2 The number of payments or period of repayment. Itemization of amount financed 102618c d. The requirements of this section apply to open-end credit plans secured by the consumers dwelling.

Regulation Z defines closed-end credit transactions as consumer credit other than open-end credit 4 Unlike open-end or revolving credit like credit cards closed-end credit usually involves a loan with a fixed repayment plan as. Thus for most closed-end mortgages. For closed end dwelling-secured loans subject to RESPA does it appear early disclosures.

10153D determine that the creditor discloses the following information about the interest rate and payments as applicable 102618s. Trigger terms when advertising a closed-end loan include. 3 The amount of any payment.

Subpart AProvides general information that applies to both open-end and closed-end credit. For a closed-end transaction secured by real property or a dwelling other than a transaction secured by a consumers interest in a timeshare plan described in 11 USC. 102660 Credit and charge card applications and solicitations.

For a closed-end transaction not subject to section 102619e and f determine whether the disclosures are accurately completed and include the following disclosures as applicable. A trigger term is an advertised term that requires additional disclosures. So what is closed-end credit.

1 The amount or percentage of any downpayment. If an advertisement promoting closed-end credit for real estate contains any of the following trigger terms the three specific disclosures listed at the bottom of this page must also be included in the advertisement. 22617 General disclosure requirements.

Accordingly the disclosures required by 102618 apply only to closed-end consumer credit transactions that are. 22618 Content of disclosures. Specifically Regulation Z dictates the treatment of credit balances how to determine APR rights of rescission and advertising.

How Closed-End Credit Works. A closed-end line. The Credit Union will provide the proper closed-end disclosures to the consumer borrower before consummation of the transaction.

102658 Internet posting of credit card agreements. The triggering terms are. 22621 Treatment of credit balances.

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

Federal Register Truth In Lending Regulation Z

Truth In Lending Act Tila Consumer Rights Protections

Understanding Finance Charges For Closed End Credit

Federal Register Truth In Lending Regulation Z

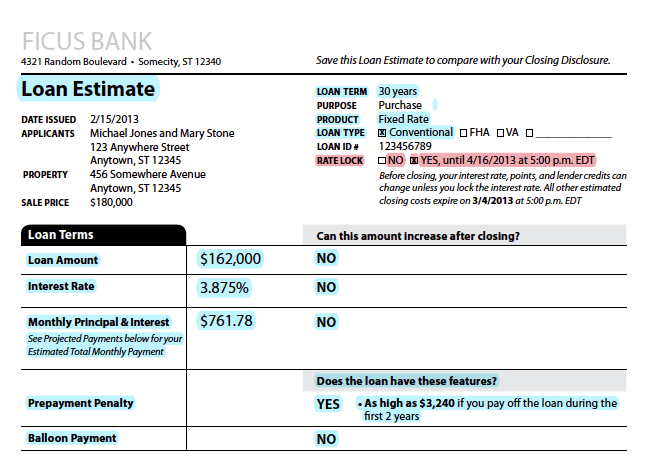

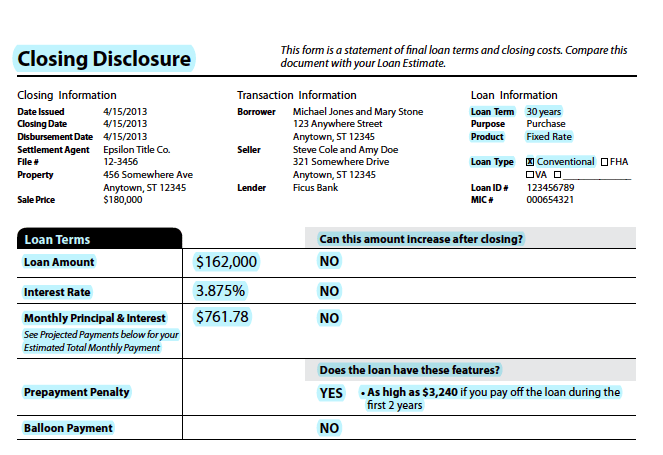

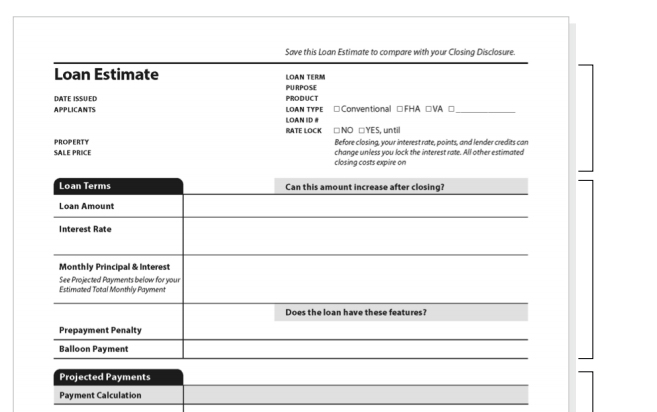

What To Know About The Loan Estimate Closing Disclosure Cd

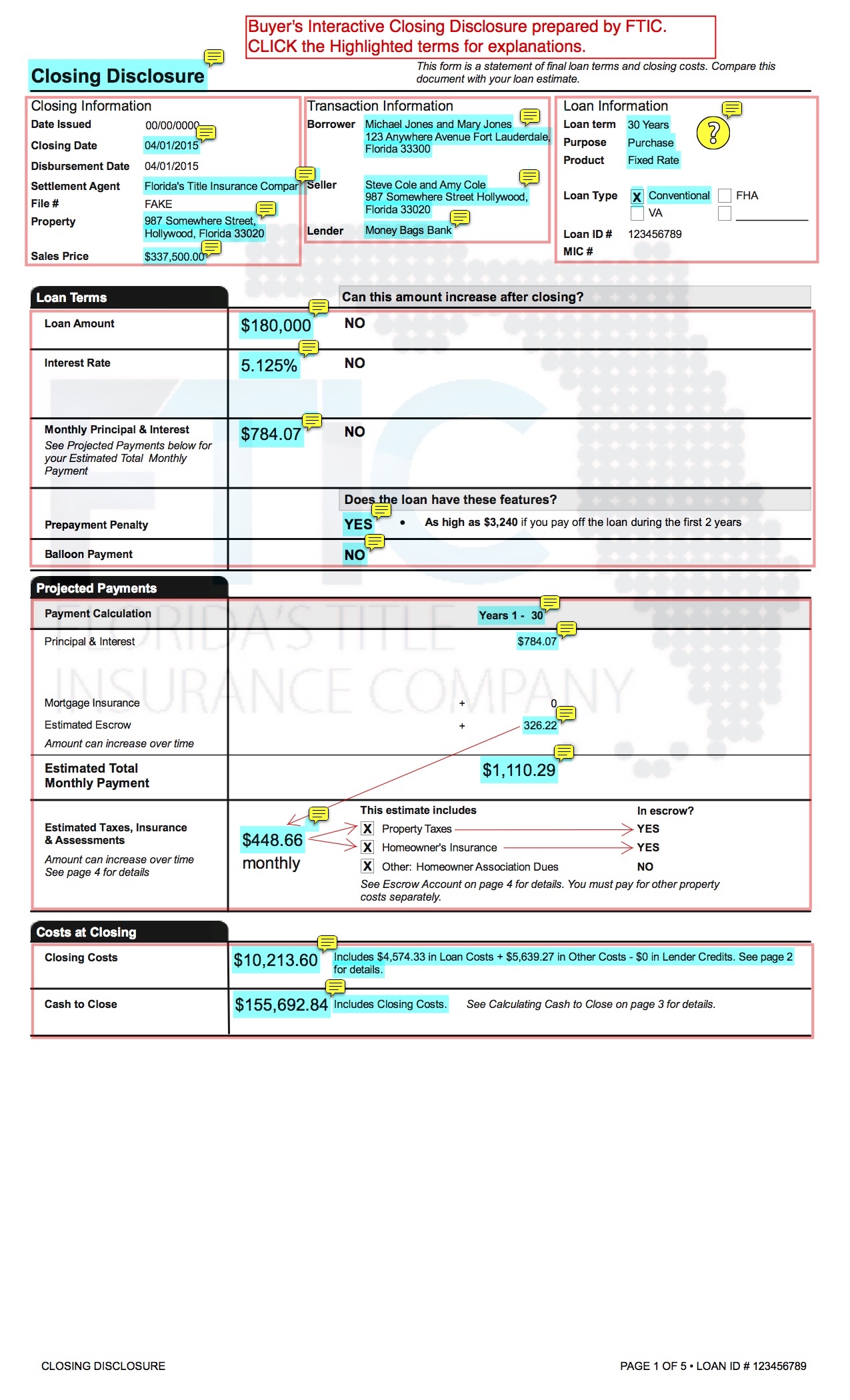

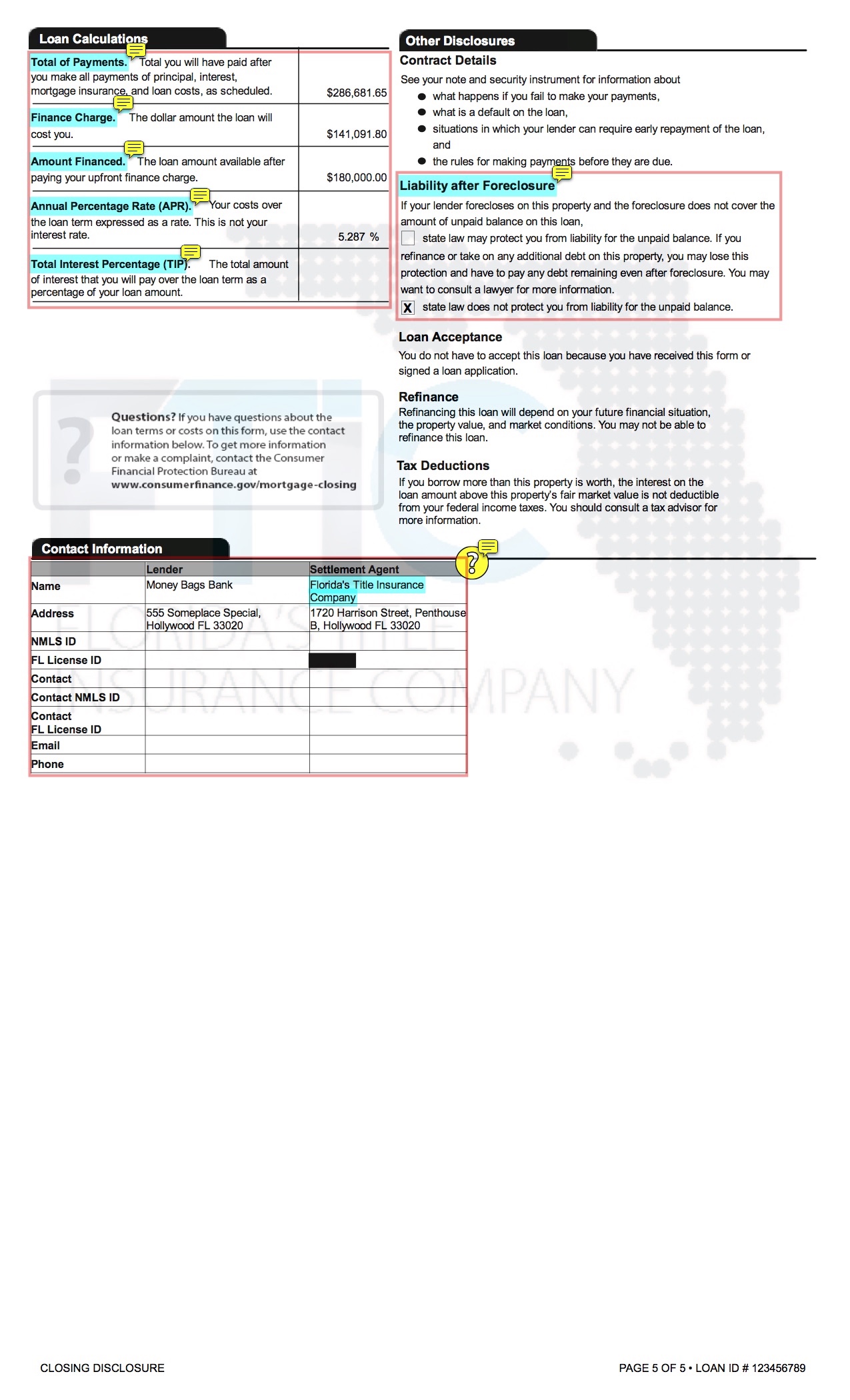

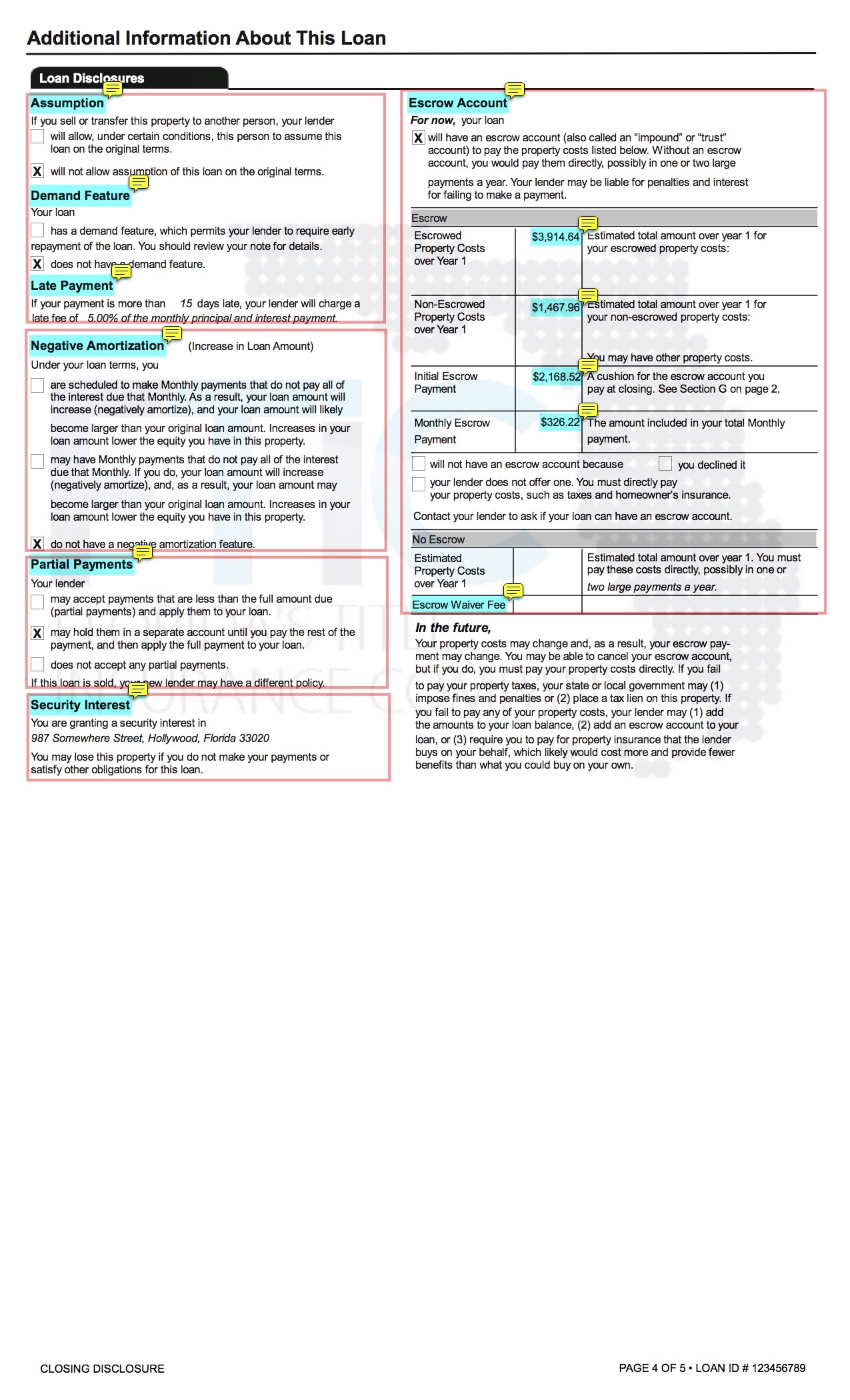

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

What To Know About The Loan Estimate Closing Disclosure Cd

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

Mandatory Disclosures To Consumer

New Mortgage Documents What Are They

Fdic Law Regulations Related Acts Consumer Financial Protection Bureau

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau

How To Read A Buyer S Closing Disclosure Florida S Title Insurance Company

Appendix H To Part 1026 Closed End Model Forms And Clauses Consumer Financial Protection Bureau